The Court of Appeals says it can

Two valuable downtown Charleston residential lots were the subject of an easement case decided by the South Carolina Court of Appeals on September 19.* Much to the dismay of the owners of 45 Lagare Street, the Court held that an appurtenant easement exists in the form of an alley that runs along a boundary of 45 Lagare Street for the benefit of 47 Lagare Street.

Master-in-Equity Mikell Scarborough had granted summary judgment in favor of the owner of 47 Lagare Street, finding an easement appurtenant burdened 45 Lagare Street, and the Court of Appeals affirmed.

In 1911, the properties were considered a single lot known as 47 Lagare Street owned by W.G. Hinson. That year, Hinson divided the property, creating 45 Lagare Street, and conveying that lot to his niece. The 1911 deed established an easement for the benefit of the 47 Lagare Street, which Hinson retained. This language established the easement:

Also, the full and free use and enjoyment as an easement to run with the land of the right of ingress, egress, and regress, in, over, through, and upon the alley-way eight (8) feet wide as a drive way or carriage way, situation, lying, and being immediately to the south of (47 Lagare), and being the southern boundary of said (47 Legare).

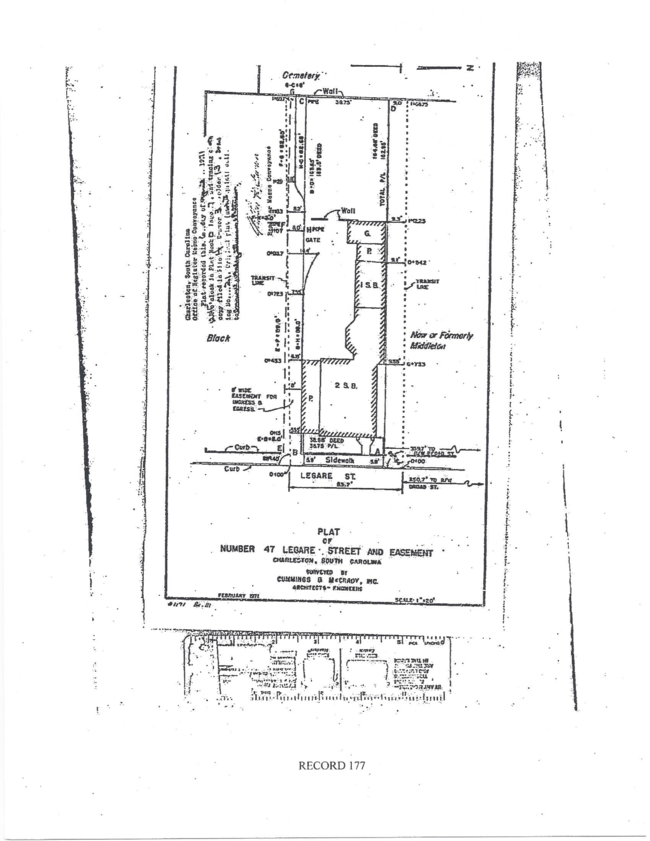

Title to both lots passed to third parties, and in 1971, a new survey was drawn,** and the owners of both properties provided verbatim descriptions of the original easement and covenanted that the no buildings or obstructions would be erected on the easement area. The documents stated that the covenants would run with the land.

The most recent deed of the benefited property recited the existence of the easement, but the most recent deed of the burdened property did not. In 2004, the owner of the benefited property added a chain-link fence and masonry wall along the border with the burdened property.

During the trial, the Appellants argued that the easement had been abandoned and stated that the only time it was used was to allow for the Respondent’s landscapers to walk down the driveway to use the gate. Respondent testified that the easement area is also used by her family members, guests, tradesmen and other permittees to access the rear of 47 Legare for large-scale appliances, equipment, and machinery and to provide access to the only suitable area for off-street parking. She also claimed that she uses the easement to access the back of her property in a golf cart.

The first issue on appeal became whether a terminus existed on 47 Legare, a requirement for an appurtenant easement. Two Supreme Court cases were discussed, Whaley v. Stevens, 21 S.C.221 (1884), which held that the terminus requirement in South Carolina only requires the dominant estate to be contiguous or adjacent to the easement. A later case, Steele v. Williams, 204 S.C. 124 (1944) held that an alleyway was an easement in gross rather than an appurtenant easement because it lacked a terminus.

The Court of Appeals found Whaley controls although no South Carolina case has explicitly defined the terminus requirement. The Court held that the terminus issue is a fact-specific inquiry and that, intuitively, the dominant estate must have access to the purported easement.

In addition, the Court stated, an appurtenant easement might be found if the purported easement (1) at least touches the dominant estate and (2) in cases where the easement is an adjacent boundary between—or runs parallel—to the dominant and servient estates, such as the case at hand, the easement does not extend beyond the dominant estate’s boundary. (At most, the easement ends at the lot line of the dominant estate.) In Steele, the alley extended beyond the appellant’s property.

The intent of the parties was held to be determinative, and the Court held that the 1911 common owner, Hinson, clearly intended that the driveway would be an easement appurtenant.

The Court next discussed the appurtenant easement requirement of necessity. 47 Legare Street obviously has direct public access on Lagare Street, but the Court held that the easement was necessary to reach the rear of the property by large-scale equipment and tools and to provide for off-street parking.

We will wait to see whether our Supreme Court has the opportunity to weigh in on this issue.

* Williams v. Tamsberg, S.C. Court of Appeals Opinion No. 5596 (September 19, 2018)

** Plat of Number 47 Legare Street and Easement surveyed by Cummings & McCrady, Inc., dated February 1971, is attached.

{kind=link}